Cancer is a dreaded disease. People often worry more about getting cancer than heart disease, the No. 1 killer more likely to take their lives. Indeed, Mutual of Omaha sent me applications for cancer coverage on several occasions. I’ve heard those policies are very profitable for insurance companies because people far over-estimate their risk of cancer. By contrast, I’ve never seen an insurance policy that only covered heart disease.

In 2022 about 1.9 million Americans were diagnosed with cancer. That same year more than 609,000 died. Of cancer deaths lung cancer is the most common accounting for 21% of deaths. Colon and rectal cancer deaths are the second most common (9%). Pancreatic cancer is third (8%), while at 7% of cancer deaths are due to breast cancer, which comes in fourth. While we’ve all heard of these four common cancers, they account for less than half (45%) of all cancer deaths. That means other cancers account for more than half (55%) of all cancer deaths.

Historically there were only a few cancer screening tests. For instance, mammography screens for breast cancer. The prostate-specific antigen test, or PSA, screens for prostate cancer. Colonoscopy identifies polyps that can turn into colon cancer, while high risk individuals who smoke may get an x-ray for lung cancer. Another cancer screening test is for cervical cancer. That leaves the vast majority of cancers not routinely screened for.

This from Wired magazine:

Of the more than 200 types of cancer, we currently only screen for cervical, breast, and bowel cancer, says Kumar. He calls this the streetlight problem: “We’re looking for cancer in the light, but four-fifths are happening in the dark.” But even if we did check for all these cancers, people aren’t going to turn up for 200 screenings. “We cannot continue the paradigm of looking for these cancers one at a time,” he says.

Cancer is usually treatable if caught early. The cancers that are the deadliest (such as pancreatic cancer) are lethal because they are difficult to catch early. Many deadly cancers have no symptoms until they’ve spread. About 90% of cancer deaths are due to metastatic cancer, that is cancer that has spread beyond the original location. In theory most cancer could be treatable if only it could be caught sooner, before it has a chance to spread.

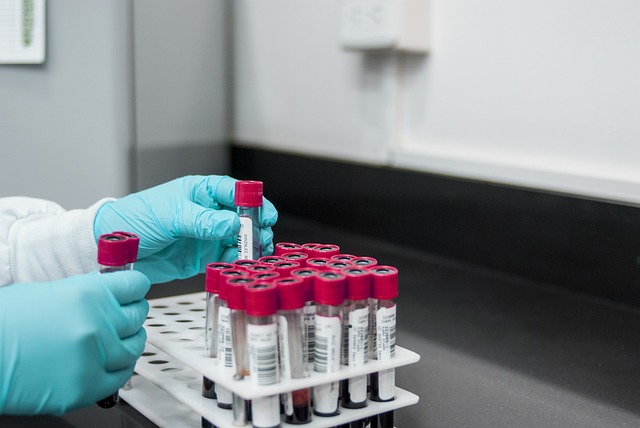

A new company named Grail has a blood test capable of detecting numerous cancers at the same time rather than testing for one at a time. It tests for cancer DNA in the blood. According to an interview by Wired magazine with Harpal Kumar president of the European branch of Grail:

The dream is a single test that can identify every cancer from a single draw of blood—and that’s roughly what Grail has been developing: a test that is sensitive to early stage cancers, can detect and locate many different cancer types, gives very few false positives, and can hone in on the most serious cancers.

Galleri is the result. The company says it can detect more than 50 types of cancer with a single blood sample. Just as regular cells shed DNA when they die, so do tumor cells, and this DNA is traceable in the blood. The test has been validated by Grail in clinical trials: If the test detects something, there’s a 45 percent likelihood that it’s cancer—an extremely high predictive rate for a cancer test. Galleri says it can predict where a cancer is in the body with 90 percent accuracy.

The test called Galleri has been available in the U.S. for about a year and a half and costs $949. That sounds like a bargain if it works. That reminds me of something that John Goodman wrote years ago (see paragraph 10), ”[W]e could spend our entire gross domestic product on healthcare in useful ways. In fact, we could probably spend the entire GDP on diagnostic tests alone—without ever treating a real disease.”

About 25 years ago the National Center for Policy Analysis published a policy report on the cost per life-year saved by various interventions. The cost varies from low-hanging fruit (cheap, highly effective interventions like seatbelts, smoking cessation and childhood immunizations) to extremely costly environmental interventions. I wonder how many Galleri tests would be required to save a year of life? I doubt if the calculation has been done. If testing is done on low-risk individuals, the cost of buying a year of life could be in the billions. Testing like this is not something that Medicare or private insurance would pay for but doesn’t mean it’s not beneficial. It could provide peace of mind to people whose family have a history of cancer or peace of mine for the worried well.

Virtually all preventive medical screening tests have a positive cost per year of life saved. That means you are spending money rather than saving money. There are virtually none that save money. Yet year after year I read where politicians or public health advocates (often the news media) argues for more preventive medical interventions as a way to lower health care spending. But that does not save money. That’s not to say prevention is a bad deal, just it does not save money. The upside of Galleri is that you may discover cancer early enough that it’s easily cured. The downside of Galleri is that you could get a false positive that requires thousands in further testing to discover you never had cancer.

You make me laugh Devon. The definition of insurance is not something that keeps you healthy. Insurance is a transfer of risk not stupidity. Insurance pays for an UNFORESEEN claim or expense. Your deciding to spend $8,000 to determine if your head is filled with tumors is not an unforeseen expense.

All of the politicians in Congress that are Obamacare (INSURANCE) experts are Medical Doctors who don’t understand insurance. I have insured lots of docs and I was never impressed with their knowledge. It is easy to tell you have never had an insurance license Devon.

I ensured 2 doctors in Colorado Springs in 2000 with MSA coverage. I took them off a “group” of docs that worked at the local hospital. The 1st doctor got bone cancer in 18 months and I got a call from him that TIME insurance company was doing a review to see if it was pre-existing. Of course it wasn’t and we spent $2.6 million and he is still alive today voting for Democrats. He lived for 6 weeks in a bubble twice. (He is so lucky he met me because he had a stroke during his 1st surgery and you can’t be an anesthesiologist after a stroke – he would have lost that group coverage)

The other doc’s husband, my friend from high school, got throat cancer but he waited until 25 months after the insurance’s Effective Date so we didn’t review for pre-existing. The review can only be done in the 1st 24 months. His cancer was cheap, cheap cheap compared to Ray’s. I think “Ray”, the 1st doc, was the most expensive client I have ever had.

I had the 28,000 stores of 7-Eleven on January 1st of 1997 for the Medical Savings Account (MSA) “Original Pilot Test” and St Louis was the 1st city we enrolled. The 1st enrollee had a heart attack so he quit smoking and his premium dropped. We lost our ass on those people in St. Louis. But next I went to Chicago and enrolled Mariana who got ovarian cancer and it took four years for her to die. But the cost was no where close to that Colorado doc.

The 1st stand alone 7-Eleven employee was a single girl with 2 children that couldn’t afford her share of the group plan that was $400 a month. I follow the law and the state law says the Individual Medical (IM) can’t be paid for by an employer, not ONE penny (No competition to group health plans right). 100% of her 1997 premium for her and the boys was $78 a month on MSA insurance. Her employer, 7-Eleven Franchisee, put $100 in her MSA monthly.

The head guy at 7-Eleven Tower in Dallas said, “If they don’t get the insurance we should fire them because we would have an IQ problem!” I told him that Hillary said the MSA was a tax dodge for the healthy and wealthy. He laughed and said, “Jay Lenno has never confused the 7-Eleven employees as being amongst the rich.”

FYI – Remember when I said an Employer couldn’t pay ONE penny of the premium? (The Law) On that 7-Eleven employee we had to debit 7-Eleven’s bank account and 7-Eleven accountants will electronically SEND money to vendors but NOBODY drafts the 7-Eleven bank account. So I had my wife, the best salesperson, get the 7-Eleven guy to agree. He was so conservative and wanted to participate so bad that he agreed.

FYI – ALSO, if you remember to go tax free with a tax-free MSA you had to be self-employed OR an employee of a small employer, less than 50 employees, on employer “SPONSORED” insurance. I got legal at TIME Insurance Company, the 1st company with MSA insurance, to AGREE with me that empolyers who debit an employees’ wages and actually paid for the insurance satisfied the definition of EMPLOYER SPONSORED INSURANCE! (WOW huh?)

I had Valley Marine a small employer who every time they hired a new employee I had to go and enroll them. I was there enrolling a new employee and this girl comes up and says, “Are you the MSA guy?” I said YES. She said, “I have more in my MSA that I do for all my other accounts added together.” I said, “How much do you have in your MSA?” She said, “$10,000.” So I asked, “How much is in all of your other accounts?” She said, “Nothing.”

Wouldn’t it have been better Devon if you told the real hisory of HSAs in America instead of your ‘Brief History Of Health Savings Accounts” in SINGAPORE! Remember, when I said the title should have been, A Brief History of TIME, the real 1st company with MSAs?

Ron I understand that insurance is a transfer of risks that are unknown. That is why I opposed Obamacare. It requires enrollees cross-subsidize known risks, which by definition are uninsurable. I was not insinuating insurance should cover cancer tests in asymptomatic people. As I noted near the end of the post, the cost per life year saved would likely be in the billions for some populations. A few years ago the threshold for cost-effective interventions were between $143,000 and $388,000 per life year gained.

The following link explains preventive medical screenings and willingness to pay. Cancer screenings have the highest willingness to pay of any screening service.

https://assets.morningconsult.com/wp-uploads/2023/03/31122512/Screen-Shot-2023-03-31-at-11.59.25-AM.png